Sushma Buildtech legal issues | Sushma Builder crisis

Introduction

The real estate sector in India has been both a promise and a peril for homebuyers. While developers advertise modern housing complexes with world‑class amenities, delays and defaults often leave families in distress. One of the most prominent cases in Punjab is the crisis surrounding Sushma Buildtech Private Limited (SBPL). This blog provides a comprehensive 2000‑word analysis of the issues faced by customers, the legal precedents, and the remedies available.

The Sushma Builder Crisis: End-to-End Analysis

The crisis surrounding Sushma Buildtech Limited, primarily centered on projects in Zirakpur and Mohali (Punjab, India), represents a multifaceted breakdown in the real estate development and delivery ecosystem. It has trapped thousands of homebuyers, financial institutions, and contractors in a prolongued period of uncertainty.

A comprehensive analysis reveals distinct stages of the crisis, their interconnected issues, and the evolving pathways toward resolution.

Background of Sushma Buildtech

Sushma Buildtech rose to prominence in Zirakpur and nearby areas with projects such as Sushma Crescent, Sushma Grande, and Sushma Joynest. The company promised timely possession, luxury amenities, and transparent dealings. However, over time, residents reported:

- Delays in possession leading to financial strain.

- Non‑delivery of promised amenities like clubhouses, swimming pools, and landscaped gardens.

- Absconding representatives leaving residents without accountability.

- Financial irregularities in maintenance funds and hidden charges.

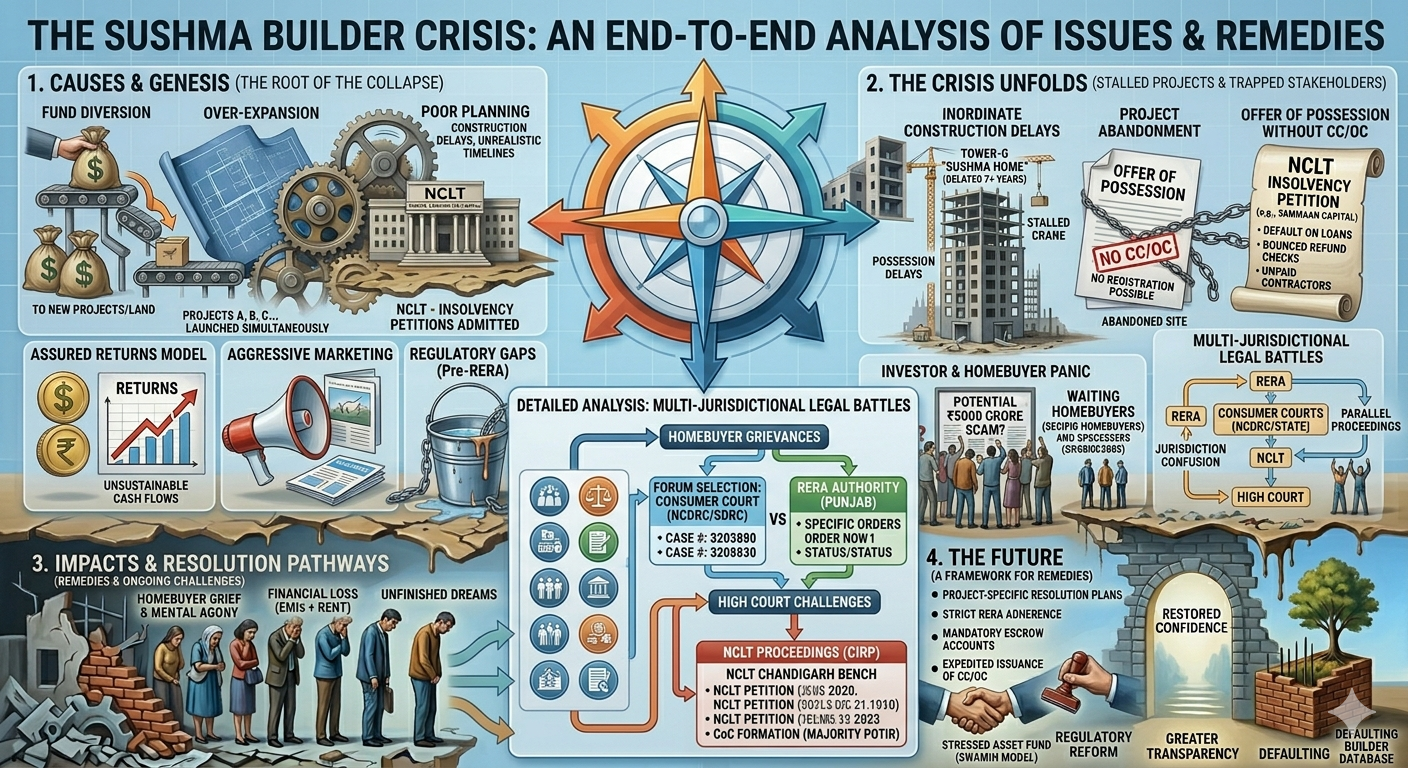

1. Causes and Genesis: The Root of the Collapse

The crisis did not happen overnight but was the result of a convergence of strategic failures, regulatory gaps, and financial mismanagement.

-

Fund Diversion and Mismanagement: A primary allegation is that funds collected from homebuyers in one project were diverted to purchase land or start new projects, rather than being utilized to complete the construction of the project for which they were intended. This created a liquidity crisis as older projects were starved of capital.

-

Over-Expansion and Aggressive Marketing: The builder launched numerous large-scale projects simultaneously, often backed by aggressive marketing and promises of “assured returns” (e.g., 12% monthly return to investors). This model relied heavily on continuous new cash flows, which became unsustainable when market conditions shifted or new sales slowed.

-

Poor Project Planning and Execution: Inadequate assessment of construction timelines, material costs, and logistical challenges led to cascading delays. Several projects are now completely stalled or progressing at a “snail’s pace.”

-

Regulatory Gaps (Pre-RERA): Many of these projects were launched before the Real Estate (Regulation and Development) Act (RERA) was strictly enforced. This allowed the builder to operate with minimal financial oversight and loose contractual obligations regarding possession timelines.

| Issue | Symbolic Representation (in image) | Description |

| Fund Diversion | Money bags tipping onto a conveyor belt. | Capital intended for construction being siphoned off. |

| Over-Expansion | Multiple, disconnected blueprints and structures. | Commencing too many projects without a stable foundation. |

| Poor Planning | Cluttered, chaotic gears and an unstable NCLT building. | Operational inefficiency and lack of strategic foresight. |

2. The Crisis Unfolds: Stalled Projects and Trapped Stakeholders

As the business model failed, the symptoms of the crisis became starkly visible, impacting all parties involved.

-

Inordinate Construction Delays and Project Abandonment: Projects like “Sushma Crescent” and “Sushma Valencia” have faced delays ranging from three to over seven years past their original contractual possession dates. In some cases, construction has been completely abandoned.

-

** possession Without Statutory Certificates:** When possession was offered in certain towers, it was often done without the mandatory Completion Certificate (CC) or Occupation Certificate (OC). Homebuyers who accepted possession under these conditions found themselves unable to register their properties or access essential services like permanent electricity and water connections.

-

Default on Financial Obligations: The builder defaulted on loans to financial institutions (like Sammaan Capital Ltd.) and failed to pay contractors and workers, leading to further work stoppages and legal actions.

-

Investor and Homebuyer Panic: The cessation of “assured return” payments, combined with construction delays and reports of a potential ₹5000 crore scam, led to widespread panic. Investors who received refund checks often found they bounced due to insufficient funds.

-

Multi-Jurisdictional Legal Battles: Homebuyers and creditors initiated proceedings simultaneously across different forums, including RERA, Consumer Courts (State and National Commissions), and the National Company Law Tribunal (NCLT) for insolvency. The parallel nature of these cases initially created confusion regarding jurisdiction and the hierarchy of remedies.

| Issue | Symbolic Representation (in image) | Description |

| Construction Delay | Skeletal tower (Tower-G) with “DELAYED” label. | Stalled projects and unfinished structures. |

| Project Abandonment | Stalled construction crane. | Complete halt of work on site. |

| Default on Loans | “NCLT Insolvency Petition” list. | Legal action by creditors for unpaid debt. |

| Worker Protests | Figures holding a “PROTEST” banner. | Contractors and workers unpaid for labor. |

3. Impacts and Path to Resolution: Remedies and Ongoing Challenges

The human and economic toll of the crisis is profound, but a structured framework for resolution is gradually emerging.

-

Severe Human Toll: Homebuyers suffer from immense mental agony and financial loss. Many are stuck paying both rent for temporary housing and Equated Monthly Installments (EMIs) for home loans on non-existent properties.

-

Judicial Intervention and Precedence: The courts have had to calibrate protection for homebuyers while maintaining the integrity of the insolvency process. Key legal precedents establish that homebuyers are “vital stakeholders” and their protection must be prioritized in insolvency proceedings, especially in real estate cases where the underlying asset (land) might be at risk of cancellation.

-

NCLT Insolvency Proceedings (CIRP): The crisis culminated in the admission of insolvency petitions against Sushma Buildtech Limited by creditors and homebuyers. This initiated the Corporate Insolvency Resolution Process (CIRP).

-

Committee of Creditors (CoC): Homebuyers, now classified as financial creditors, form the majority of the CoC and have the power to vote on a Resolution Plan to revive the company and complete projects.

-

Successful Resolution vs. Liquidation: The optimal outcome is the approval of a viable resolution plan by a new developer. If no plan is approved, the company faces liquidation, which would be catastrophic for homebuyers as assets would be sold to pay off secured creditors first.

-

-

Balanced High Court Orders: A recent significant development is an order by the Punjab and Haryana High Court to unfreeze the builder’s bank accounts. This was a pragmatic decision based on the builder’s undertaking to refund 50% of the principal amount to certain homebuyers within a strict 6-month timeline. The court reasoned that a total freeze prevented the builder from generating funds for either construction or repayment.

| Remedy/Impact | Symbolic Representation (in image) | Description |

| Homebuyer Grief | Line of people looking downcast (“MENTAL AGONY”). | The human cost of waiting and financial strain. |

| CIRP | Arrows pointing to NCLT, CoC, and Resolution Plan. | The structured legal pathway for corporate revival. |

| Partial Refund | Scales tipping toward a small bag of money (“50% UNDERTAKING”). | Court-mandated interim financial relief for buyers. |

| Project Completion | An archway with “RESTORED CONFIDENCE” and a thriving tree. | The ultimate goal: delivery of homes and regulatory reform. |

4. The Future: A Framework for Remedies

An “end-to-end” solution requires a comprehensive, multi-pronged approach that moves beyond reactive legal battles.

-

Project-Specific Resolution Plans: The NCLT process must focus on project-wise resolution rather than treating the company as a single entity, as different projects are at different stages of completion and have different viability.

-

Strict Adherence to RERA: The Punjab RERA must strictly enforce provisions for mandatory escrow accounts for each project, ensuring 70% of collections are used solely for construction.

-

Expedited Issuance of CC/OC: The state government and local municipal bodies (like MC Zirakpur) must create a special fast-track mechanism for the inspection and issuance of statutory certificates for buildings that are functionally complete but stuck on administrative hurdles.

-

Creation of a “Stressed Asset” Fund: A dedicated fund, potentially modeled after the central government’s SWAMIH fund, should be established by the state to provide last-mile funding to complete viable, but stalled, real estate projects.

-

Regulatory Reform and Greater Transparency: Stricter due diligence of developers before project registration, mandatory quarterly progress reports on RERA websites, and a public database of defaulting builders are essential to prevent future crises.

Key Issues Faced by Customers

Delayed Possession

Thousands of families faced double financial burdens—paying EMIs and rent simultaneously.

Missing Amenities

Marketing brochures highlighted luxury features, but many remained incomplete years after possession.

Builder Absconding

In some cases, builder representatives disappeared, creating a vacuum in management.

Financial Mismanagement

Residents alleged misuse of funds and arbitrary charges.

Legal Complexity

Individual buyers struggled to pursue lengthy legal battles, weakening their bargaining power.

Legal Precedents

Supreme Court – Padmini Infrastructure v. Royal Garden RWA (2021)

The Court ordered handover of possession to the RWA and compensation of ₹60 lakh, recognizing RWAs as legitimate entities.

State Consumer Commission – RWA vs Barnala Realtech (2024)

The Commission upheld the RWA’s right to represent residents collectively.

Punjab & Haryana High Court – Sushma Crescent Cases (2024–25)

Multiple petitions led to directions for refunds and completion of construction.

Importance of RWAs

Benefits

- Legal standing to sue builders collectively.

- Management control over common areas.

- Transparency in community finances.

- Stronger negotiating power.

Steps to Form an RWA

- Register under the Societies Registration Act, 1860.

- Draft bylaws.

- Elect office bearers.

- Document builder defaults.

- File collective complaints.

Legal Remedies Available

Consumer Protection Act

Allows complaints for refunds, compensation, and enforcement of amenities.

RERA

Mandates timely possession and transparency, enabling penalties and refunds.

Civil Courts / High Court

Can order refunds, asset freezes, or transfer of management rights.

Criminal Complaints

Fraud or misappropriation can lead to FIRs and police investigations.

Practical Steps for Customers

- Document Evidence: Agreements, receipts, and photographs.

- Unite Residents: Form or join an RWA.

- Set Deadlines: Give builders one last chance.

- File Complaints Collectively: Approach consumer courts or RERA.

- Seek Compensation: Demand refunds and damages.

- Engage Media: Public pressure accelerates resolution.

Risks and Challenges

- Builder insolvency may limit recovery.

- Legal delays can be lengthy.

- RWAs require active participation.

- Litigation costs can be significant.

Case Study: Hypothetical Action Plan

Residents of Sushma Crescent form an RWA, document defaults, and set a deadline. When the builder fails, they file collective complaints in Consumer Court and RERA. Media coverage adds pressure, leading to court orders for refunds or completion. The RWA takes over maintenance, ensuring transparency.

Lessons for Homebuyers

- Conduct due diligence before investing.

- Understand rights under RERA and Consumer Protection Act.

- Value community unity.

- Maintain documentation.

Conclusion

The Sushma Builder crisis highlights the importance of unity and legal preparedness. Customers must form RWAs, document defaults, and pursue structured legal remedies. Courts have sided with residents when builders fail to deliver. Though the path is long, persistence ensures justice and security for homebuyers.