UPI vs Alipay

UPI vs Alipay: Two Payment Giants, Two Different Philosophies

Ever wondered why India and China, both digital powerhouses, built completely different payment ecosystems?

🇮🇳 India chose openness.

🇨🇳 China chose integration.

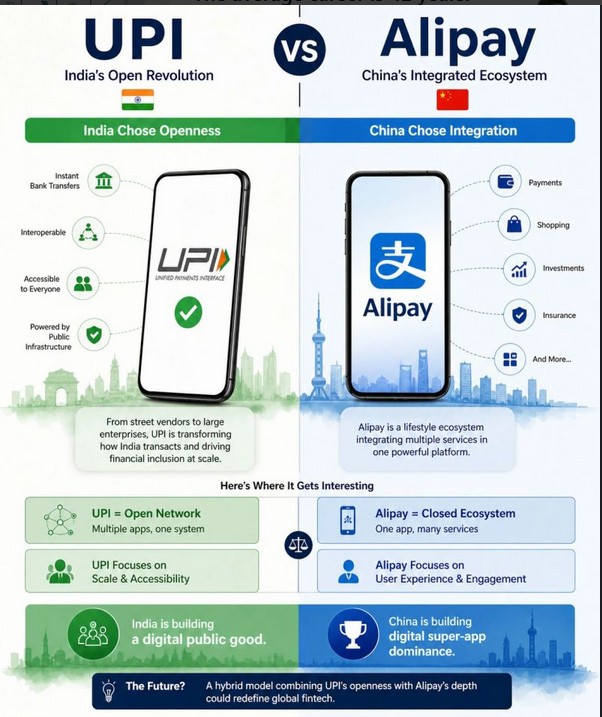

Comparing UPI (Unified Payments Interface) and Alipay provides a fascinating look at two different philosophies of digital finance: one built as a public utility and the other as a private ecosystem.

Both have become global benchmarks in 2026, but they are based on fundamentally different architectures.

UPI (Unified Payments Interface) is a national digital infrastructure for instant bank-to-bank transfers, simple and interoperable, accessible to all. It has changed the way India does business, from street vendors to big businesses, taking financial inclusion to the next level.

Alipay is not only a payment app, but also a lifestyle ecosystem. Developed by Ant Group, it combines payments, shopping, investments, insurance and more into a single powerful platform.

Now here’s where it gets interesting:

UPI = Open network → multiple apps, one system

Alipay = Closed ecosystem → one app, many services

1. The Core Philosophy

-

UPI (The Open Highway): UPI is a public infrastructure. It’s not an app; it’s a protocol built by the NPCI (National Payments Corporation of India). It allows any bank and any third-party app (like Google Pay, PhonePe, or BHIM) to talk to each other.

-

Alipay (The Walled Garden): Alipay is a private platform. It originated as an escrow service for Alibaba’s e-commerce sites. While it has expanded massively into a “Super App,” it remains a closed-loop system where both the merchant and the user traditionally need an Alipay account to interact within its ecosystem.

2. Fund Management

-

Direct Bank to Bank (UPI) : In a UPI transaction, the money gets transferred instantly from your bank account to the recipient’s bank account. There is no middleman.

-

Digital Wallet (Alipay) Alipay is primarily a stored-value wallet. Typically you “top up” your Alipay balance from your bank, and the money sits in the alipay ecosystem until you spend it or withdraw it back to your bank.

3. Interoperability

-

UPI: High interoperability. You can scan a PhonePe QR code with a Google Pay app and it works seamlessly because they all use the same underlying language (UPI).

-

Alipay: Traditionally low interoperability. While there has been recent regulatory pressure in China to allow “interconnectivity” between different platforms (like WeChat Pay), it is not natively built as a shared public rail in the same way UPI is.

4. Revenue Model

-

UPI: For a long time, UPI was essentially free for users and merchants (Zero MDR), funded by the government and banks to drive financial inclusion. Even as it evolves, it remains one of the cheapest ways globally to move money.

-

Alipay: As a private business, Alipay generates significant revenue through merchant fees, credit services (like Huabei), and wealth management products within the app.

5. At a Glance: Comparison Table (2026 Data)

| Feature | UPI (India) | Alipay (China) |

| Model | Open-loop (Interoperable) | Closed-loop (Proprietary) |

| Storage | Directly in Bank Account | Digital Wallet / Balance |

| Global Rank | #1 in Real-time Payments (49% Global Share) | Major Player in Mobile Wallets |

| Primary Use | High-frequency retail (P2M & P2P) | E-commerce, Lifestyle & Credit |

| Ownership | Government-backed (NPCI) | Private (Ant Group) |

UPI focuses on scale & accessibility

Alipay puts emphasis on user experience & engagement

Both models are successful but for very different reasons

India is creating a digital public good.

China is creating dominance for digital super apps.

Both models provide valuable insights:

India shows how public digital infrastructure can grow inclusively, and China demonstrates the strength of platform ecosystems in boosting user experience.

Trends Today (2026)

Interestingly, the two are starting to meet in the middle. Recent reports suggest that Alipay+ (international arm of Alipay) is in talks to integrate with UPI. This would mean an Indian traveler in a Southeast Asian mall could scan an Alipay+ QR code and pay using their UPI app in Indian rupees, the ultimate “best of both worlds” scenario for global digital finance.

#Fintech #DigitalPayments #UPI #GlobalFinance #PaymentInfrastructure #Innovation #SystemDesign